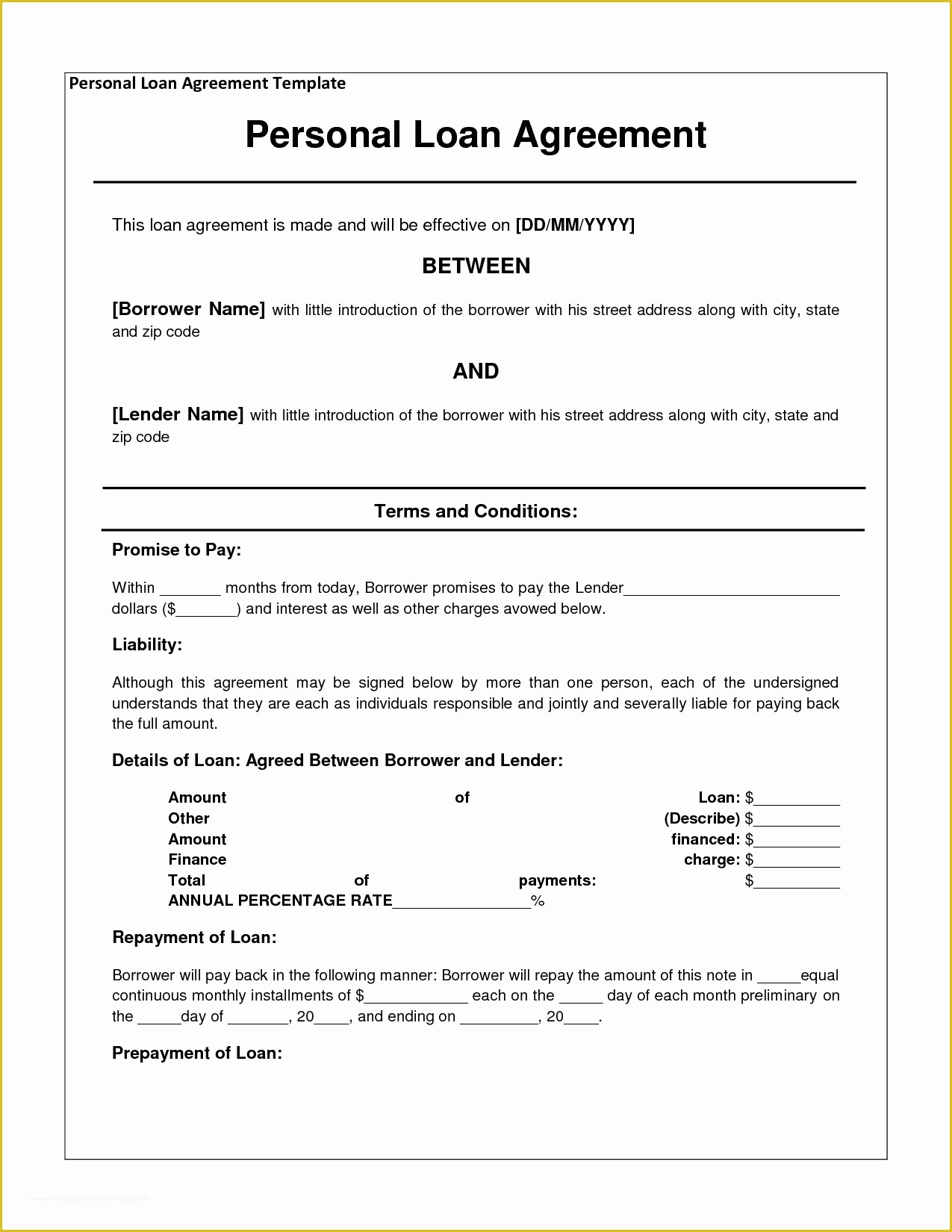

Creating a legally sound and comprehensive Personal Loan Repayment Agreement is a crucial step in securing your financial future. A well-drafted agreement protects both you and your lender, ensuring clarity and minimizing potential disputes. This guide provides a template and essential considerations for crafting a robust agreement. Personal Loan Repayment Agreement Template is the cornerstone of responsible loan management. It’s more than just a document; it’s a roadmap for a successful repayment relationship. Understanding the nuances of this agreement is paramount to maintaining a positive standing with your lender and avoiding costly complications. This template offers a solid foundation, but it’s always recommended to consult with a legal professional to ensure it aligns with your specific circumstances and local laws.

The process of creating a Personal Loan Repayment Agreement begins with a thorough understanding of the loan terms and your financial obligations. This includes the loan amount, interest rate, repayment schedule, and any associated fees. Clearly defining these elements upfront will prevent misunderstandings down the line. A poorly drafted agreement can lead to significant financial strain and legal battles. Therefore, investing time and effort into creating a professional and legally sound agreement is a wise investment. Consider seeking legal advice to ensure compliance with all applicable regulations.

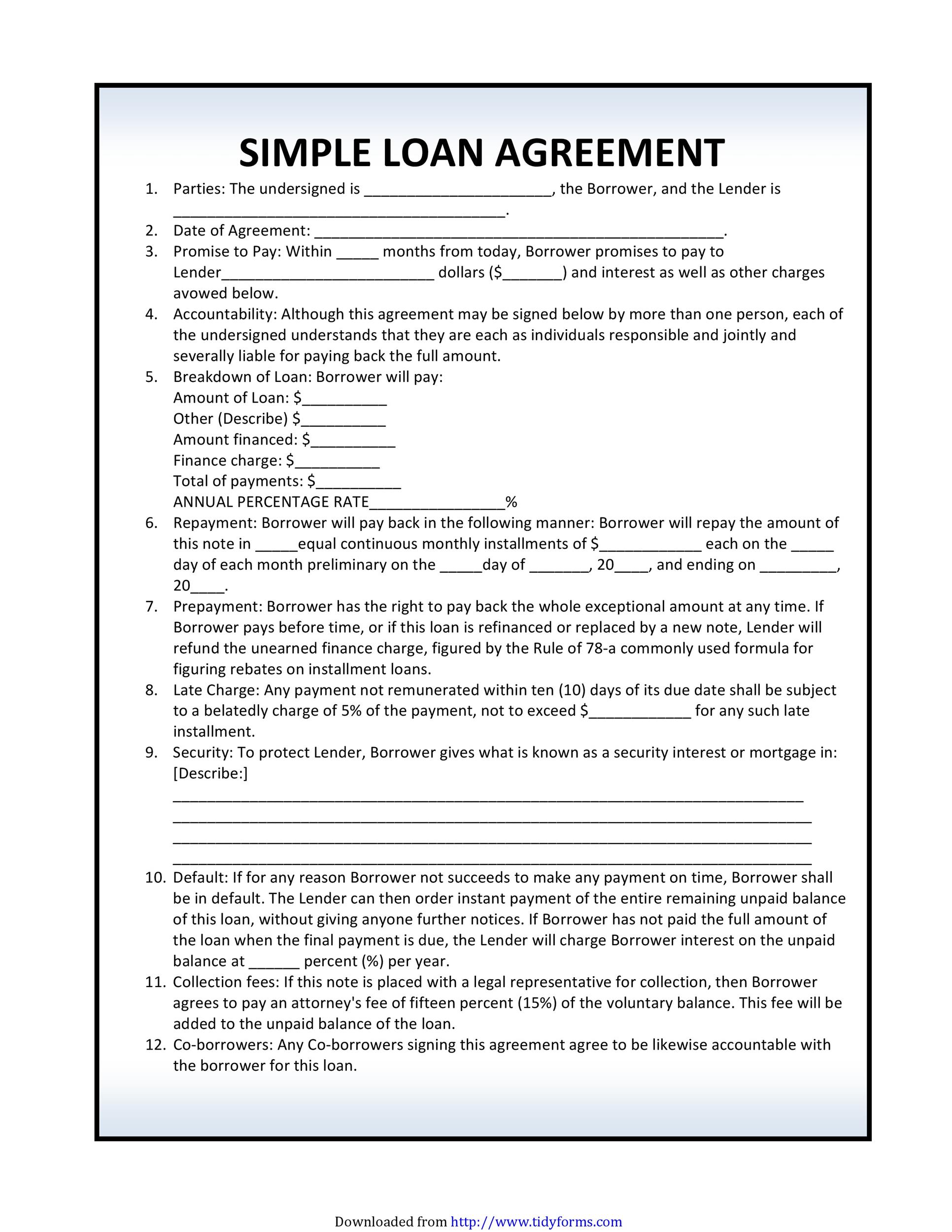

A comprehensive Personal Loan Repayment Agreement typically includes several key sections. These sections outline the responsibilities of both the borrower and the lender, establishing clear expectations and outlining the process for repayment. Let’s break down some of the most important components:

The first section should clearly define all the details of the loan, including the principal amount, interest rate (fixed or variable), loan term (length of the repayment period), and any associated fees. It’s vital to specify the exact date the loan begins and ends. This section also clarifies the currency used for the loan. For example, “The loan amount is $10,000.00, and the interest rate is 8.5% annually, calculated as a fixed rate.” This specificity is crucial for avoiding ambiguity. Furthermore, the agreement should detail the payment frequency – monthly, bi-weekly, or other schedules.

This section outlines how and when the borrower will make payments. It should specify the exact payment amount, due date, and acceptable payment methods (e.g., online transfer, check, wire transfer). It’s important to clearly state the consequences of late payments, including late fees and potential impact on credit score. The agreement should also address any potential adjustments to the repayment schedule due to unforeseen circumstances. For instance, “In the event of a significant change in income, the borrower agrees to notify the lender within 30 days of the change.”

A clear and concise late payment policy is essential. The agreement should specify the consequences of late payments, including late fees, suspension of credit, and potential legal action. It’s advisable to state a grace period for late payments, allowing the borrower a reasonable amount of time to rectify the situation. “Late payments will be subject to a late fee of $50.00, which will be added to the outstanding balance. The borrower will be required to provide a written explanation for the late payment within 5 days of the due date.”

Beyond the standard repayment schedule, the agreement should also address various options for borrowers. Some lenders offer flexible repayment plans, such as extended repayment terms or reduced payments. The agreement should clearly outline these options and their associated terms and conditions. It’s important to understand the lender’s policies regarding these arrangements. For example, “The borrower may elect to extend the repayment term by 12 months, subject to approval by the lender. In this case, the interest rate will be adjusted accordingly.” Transparency is key here.

This section outlines the lender’s rights if the borrower defaults on the loan. It should specify the remedies available to the lender, which may include legal action, collection agencies, and the possibility of foreclosure. It’s crucial to clearly define the lender’s right to pursue legal action to recover the outstanding debt. “In the event of default, the lender may initiate legal proceedings to recover the outstanding loan balance, including court costs and attorney fees.” It’s also important to note that the agreement should outline the borrower’s rights to dispute the lender’s actions.

Several clauses are particularly important when drafting a Personal Loan Repayment Agreement. These include:

A detailed explanation of how the interest rate is calculated is crucial. The agreement should clearly state the formula used to determine the interest rate, including any applicable compounding periods. “The interest rate is calculated based on the loan amount, the interest rate, and the loan term.”

A clear process for resolving disputes should be outlined. This may include mediation or arbitration. “Any disputes arising from this agreement will be resolved through mediation before resorting to litigation.”

Specify the jurisdiction whose laws will govern the agreement. This is important for determining which court has jurisdiction over any legal disputes. “This agreement shall be governed by the laws of the State of [State Name].”

The agreement should clearly state how the agreement can be amended or modified. It should specify the process for making changes, such as a written agreement signed by both parties. “Amendments to this agreement shall be in writing and signed by both the borrower and the lender.”

Understanding your rights as a borrower is essential. A well-drafted agreement protects your interests and provides a framework for resolving any disputes. Don’t hesitate to seek legal advice if you have any questions or concerns about the agreement. It’s always better to err on the side of caution. Remember, a clear and comprehensive agreement is a valuable tool for managing your Personal Loan responsibly.

Creating a robust Personal Loan Repayment Agreement is a significant undertaking, but it’s a vital investment in your financial well-being. By carefully considering all the key components outlined in this guide, you can ensure that your agreement is legally sound, protects your interests, and promotes a successful repayment relationship. The template provided offers a starting point, but remember to tailor the agreement to your specific circumstances and seek professional legal advice when necessary. Ultimately, a well-crafted agreement fosters trust and stability in your financial dealings. Proper planning and attention to detail are key to navigating the complexities of personal loans and achieving long-term financial security. Don’t underestimate the importance of a legally sound agreement – it’s a cornerstone of responsible borrowing.