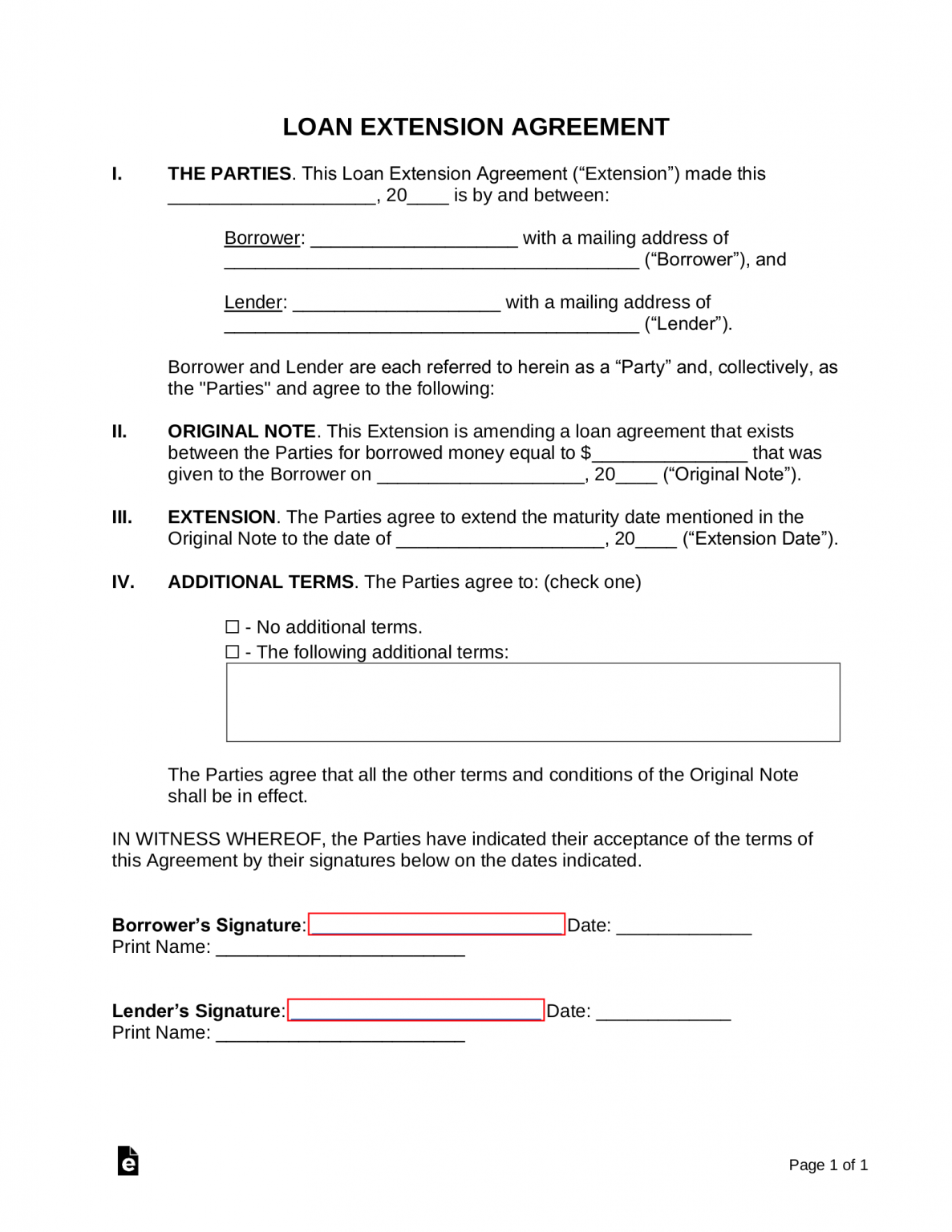

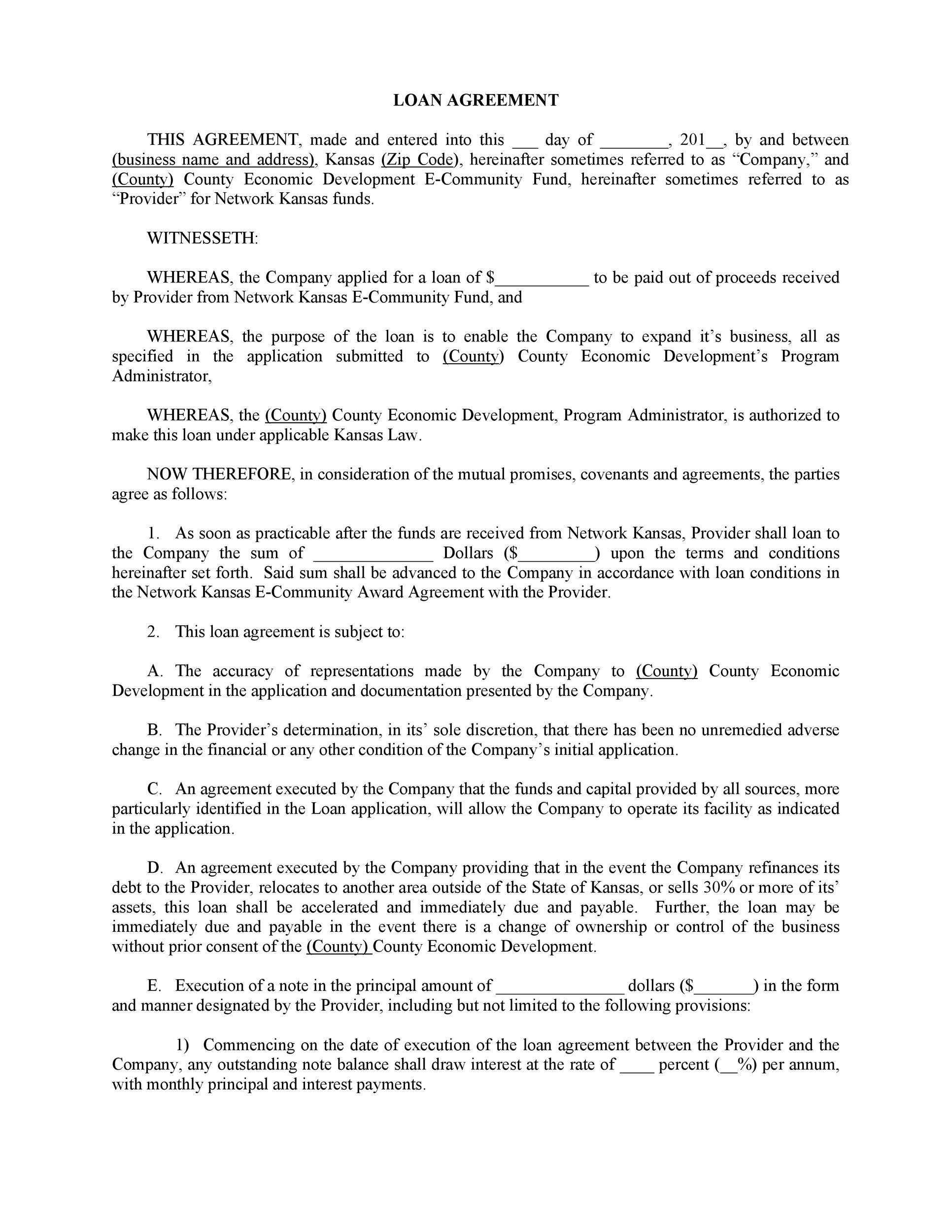

Promissory notes are a fundamental tool in business and personal finance, outlining a debt obligation between two parties – a borrower (the “principal”) and a lender (the “debtor”). They provide a clear and legally binding agreement specifying the terms of repayment, interest rates (if any), and consequences of non-payment. Understanding how to create and utilize effective promissory notes is crucial for ensuring financial stability and minimizing potential disputes. This guide will delve into the key aspects of creating and managing promissory notes, offering a comprehensive overview for both individuals and businesses. Promissory Notes Templates are readily available, and this article will explore various options and best practices for crafting a robust and legally sound document.

The core of a promissory note is its ability to clearly define the obligations of both parties. It’s not just a simple agreement; it’s a legally enforceable contract. A well-structured note protects both the borrower and the lender, providing a framework for resolving potential disagreements. The process of creating a promissory note involves several key steps, from initial planning to final execution. It’s highly recommended to consult with a legal professional to ensure the note complies with all applicable laws and regulations. Properly drafted notes can significantly reduce the risk of legal complications and safeguard your financial interests.

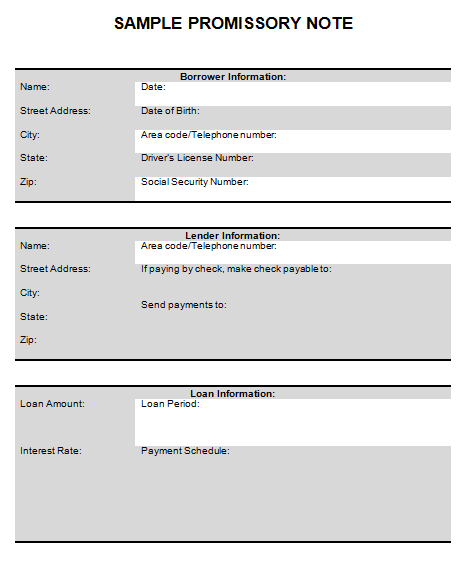

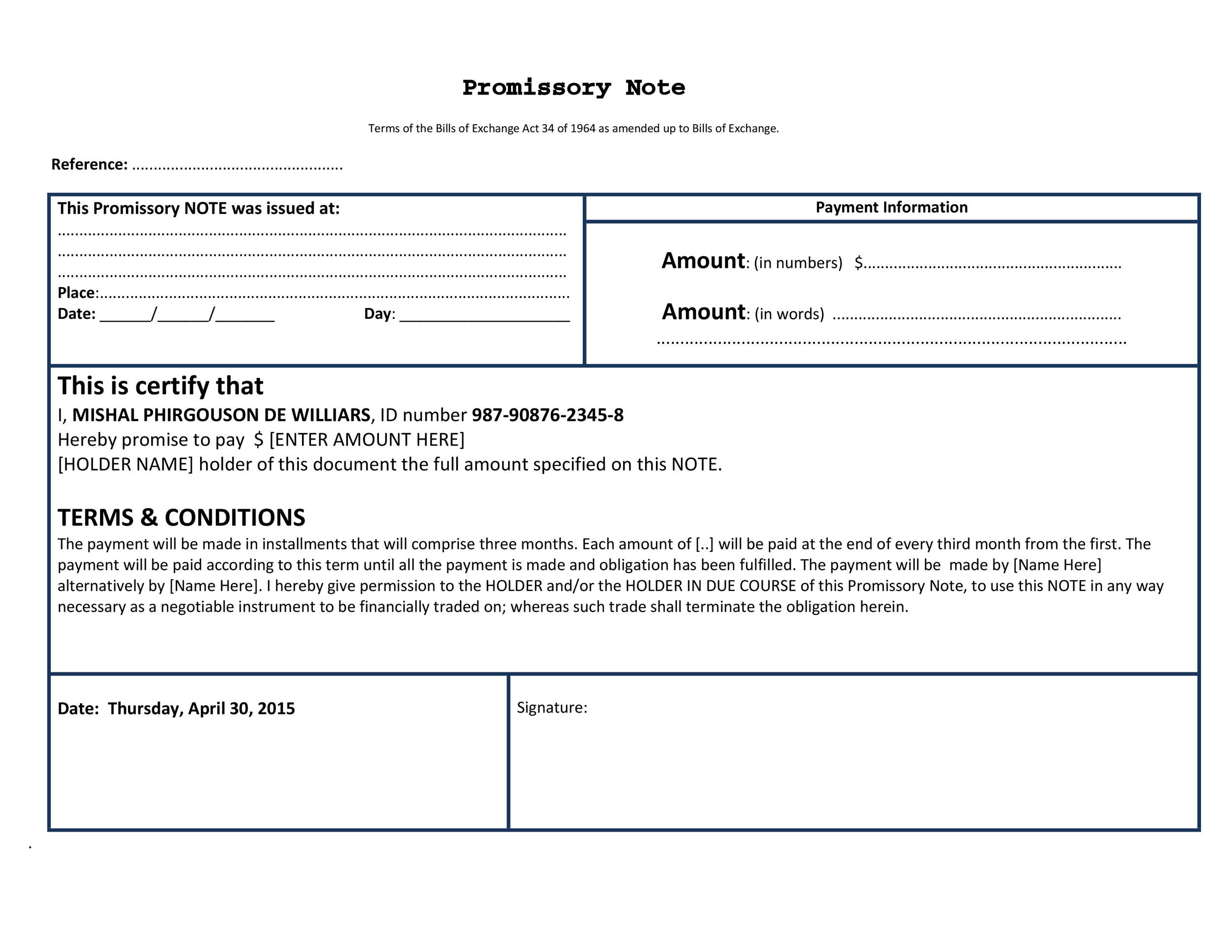

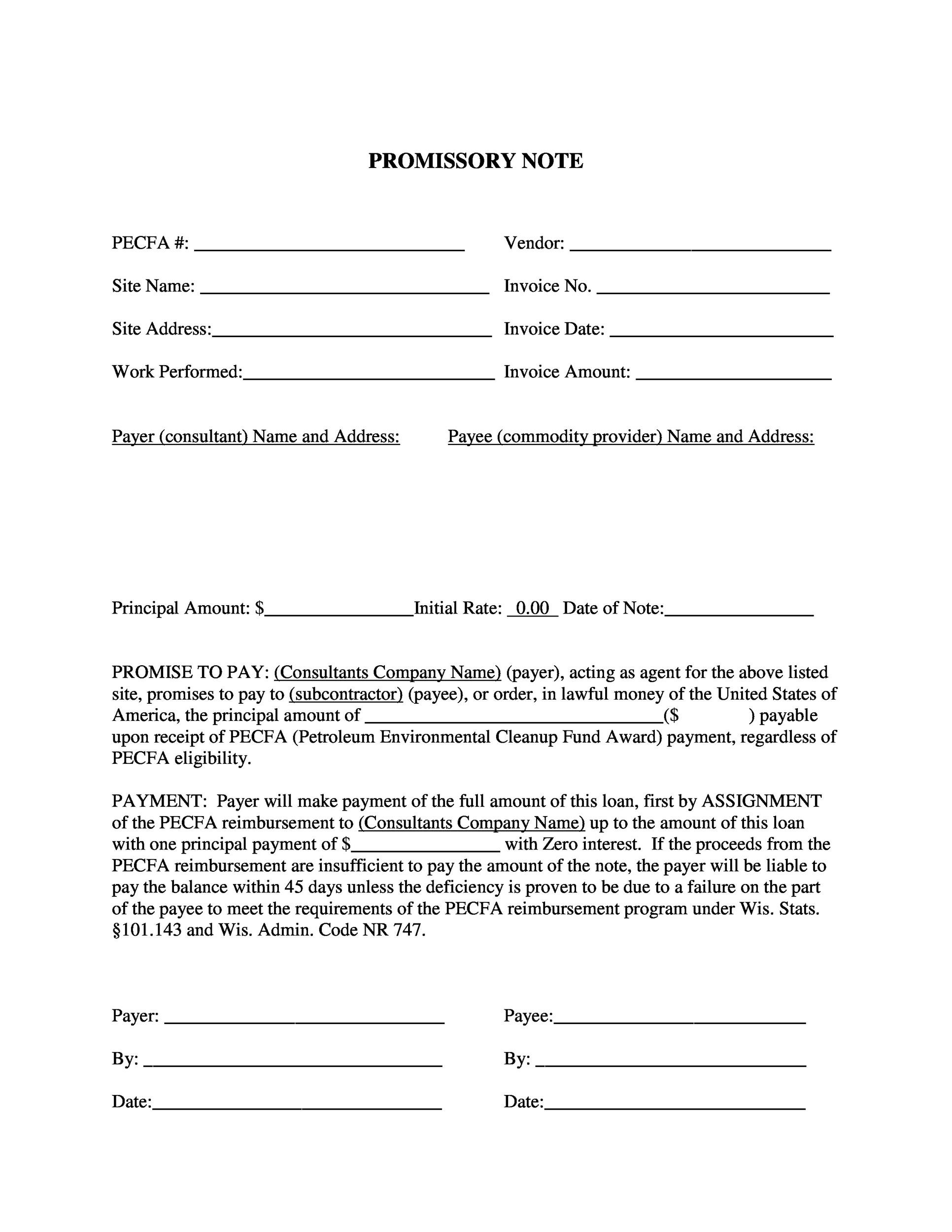

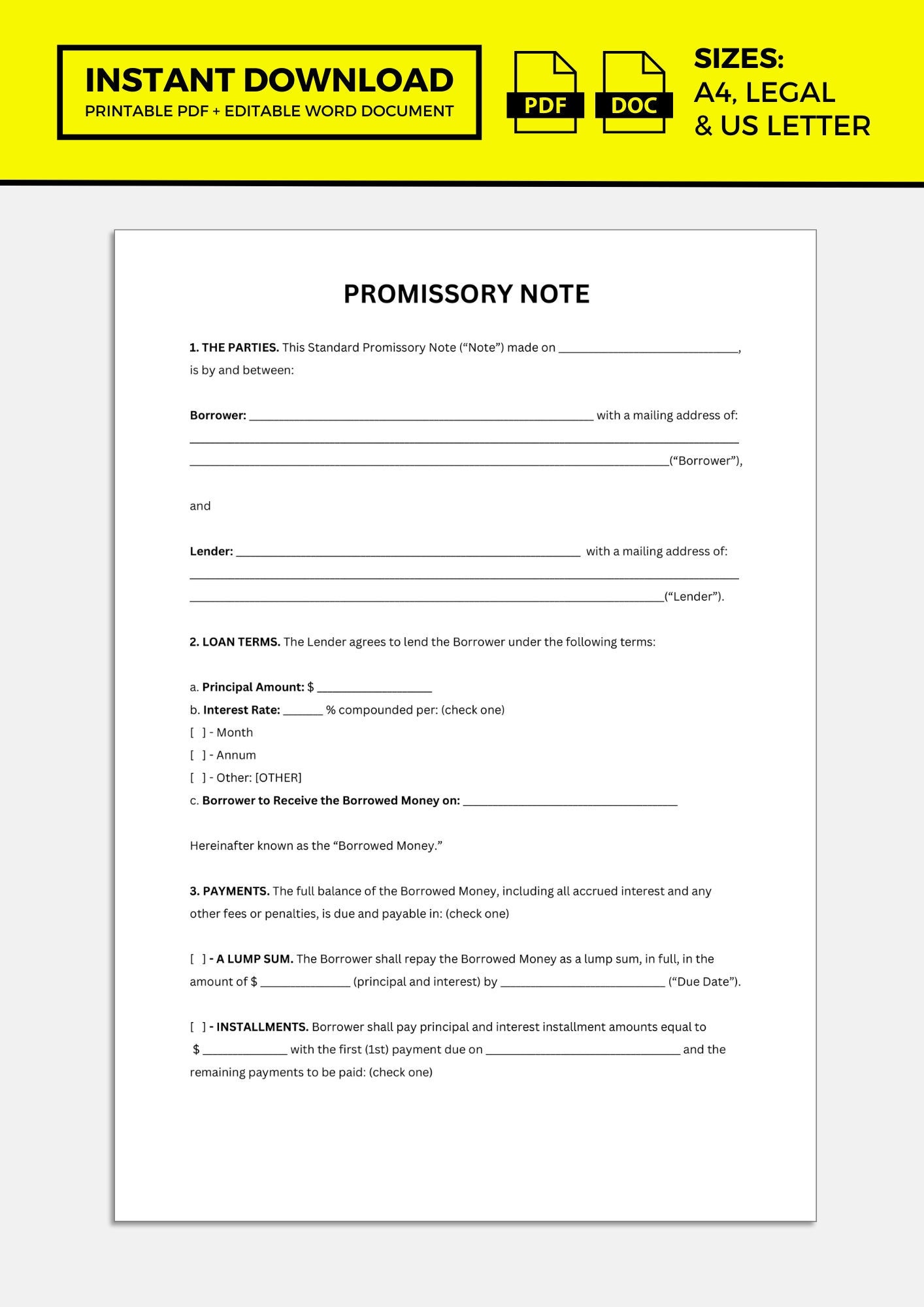

Before diving into the specifics of creating a template, it’s important to grasp the fundamental elements of a promissory note. At its heart, a promissory note is a written promise to pay a specific sum of money, usually at a specified date, to a lender. The note specifies the amount owed, the interest rate (if any), the payment schedule, and the consequences of default. Different types of promissory notes exist, each tailored to specific needs and circumstances. Understanding these variations is key to selecting the appropriate template for your situation. The clarity and detail within the note are paramount to its effectiveness.

Let’s break down the essential components of a typical promissory note:

Creating a professional-looking and legally sound promissory note requires careful attention to detail. Here’s a step-by-step guide:

Before you begin, clearly define the purpose of the note. Is it for a specific loan, a business investment, or a personal debt? The scope of the note should align with the intended use. Consider all potential scenarios and anticipate any future needs.

Numerous promissory note templates are available online. These templates can serve as a starting point, but it’s crucial to customize them to fit your specific circumstances. Popular sources include legal websites, business resource centers, and online templates. However, always review and adapt the template to ensure it meets your specific requirements.

This is where the real work begins. Carefully fill in each section of the template, ensuring accuracy and completeness. Pay close attention to the payment schedule and repayment date. Don’t underestimate the importance of a clear and concise description of the loan.

Consider adding clauses to address specific situations, such as:

Promissory notes are increasingly utilized in business financing. For startups and small businesses, they provide a straightforward way to secure funding. They can be used to finance equipment purchases, working capital, or other business expenses. For larger corporations, promissory notes are often used to secure loans for expansion, acquisitions, or other significant investments. The key is to structure the note in a way that protects the lender’s interests while providing the borrower with the necessary capital. Properly drafted notes can significantly streamline the financing process and reduce the risk of disputes.

Once a promissory note is created, it’s essential to manage it effectively. Maintain a record of all payments and outstanding balances. Use a spreadsheet or accounting software to track the note’s status. Regularly review the note with your lender to ensure compliance and address any potential issues. Promptly addressing any discrepancies or disputes is crucial for maintaining a positive relationship with your lender.

While it’s possible to create a promissory note yourself, it’s strongly recommended to seek legal counsel. A lawyer can ensure the note is legally sound, protects your interests, and minimizes the risk of disputes. They can also advise you on the best way to structure the note to meet your specific needs. The cost of legal advice is a worthwhile investment to safeguard your financial future.

Promissory notes are a vital tool for managing debt and securing financial resources. By understanding the key components, following a structured process, and seeking professional guidance, you can create effective promissory notes that protect your interests and foster strong relationships with your lenders. Remember that clear communication, meticulous attention to detail, and legal compliance are paramount to the success of any promissory note. Promissory Notes Templates are a valuable starting point, but they should always be adapted to your unique circumstances. Investing in a well-crafted note is an investment in your financial well-being.