Navigating the complexities of business finance often requires strategic borrowing, and for Australian small businesses, a Division 7a Loan Agreement Template can be a crucial tool. This agreement facilitates loans from a company to its shareholders (or their associates), ensuring compliance with Australian Taxation Office (ATO) regulations. Without proper documentation and adherence to the Division 7a rules, these loans can be reclassified as unfranked dividends, leading to significant tax implications. Understanding the nuances of these loans and utilizing a well-drafted template is paramount for both the company and the shareholder. This article will delve into the intricacies of Division 7a loans, the importance of a robust agreement, and what to look for in a suitable template.

Division 7a was introduced to prevent shareholders from accessing company profits as loans, effectively avoiding the higher tax rates applicable to dividends. The ATO closely scrutinizes these arrangements, and non-compliance can result in penalties and the loss of tax benefits. A properly structured loan, governed by a comprehensive agreement, demonstrates genuine borrowing and repayment intentions, safeguarding against adverse tax consequences. It’s not simply about having a document; it’s about ensuring the agreement reflects a commercially reasonable arrangement.

The benefits of utilizing a Division 7a loan extend beyond tax optimization. They can provide shareholders with access to funds for personal investments or expenses, offering flexibility in financial planning. However, these benefits are contingent upon strict adherence to the ATO’s guidelines, including minimum interest rates, repayment schedules, and loan terms. Failing to meet these requirements can negate the advantages and trigger unwanted tax liabilities.

Division 7a of the Income Tax Assessment Act 1997 governs loans made by a private company to its shareholders or their associates. These loans are treated differently for tax purposes than loans made to unrelated parties. The ATO views these loans as potential distributions of company profits, and therefore subjects them to specific rules to ensure fair taxation. The core principle is that if a loan is not genuinely a loan – meaning it lacks commercial terms and a clear intention for repayment – it will be reclassified as a dividend.

Several key requirements must be met to ensure a Division 7a loan remains compliant. These include:

The consequences of non-compliance with Division 7a rules can be severe. The ATO may reclassify the loan as an unfranked dividend, which is subject to tax at the shareholder’s marginal tax rate. Additionally, the company may be denied deductions for interest paid on the loan. Penalties and interest charges may also apply. Therefore, meticulous attention to detail and adherence to the ATO’s guidelines are crucial.

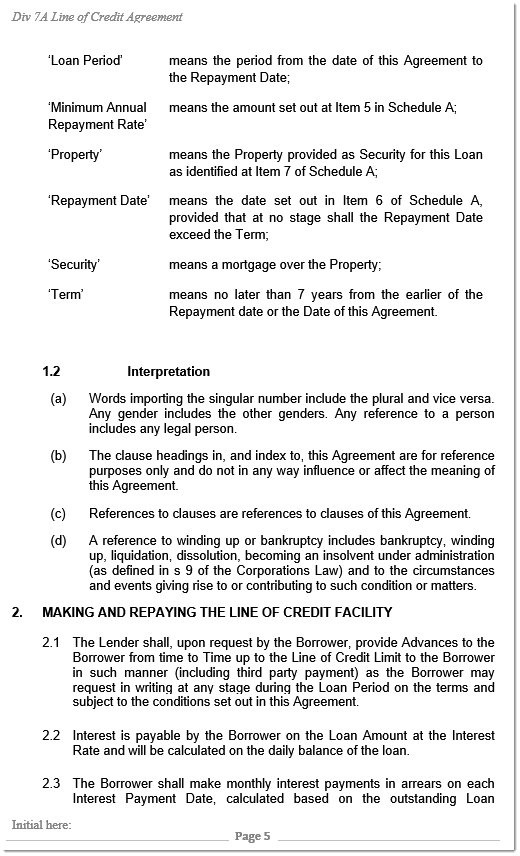

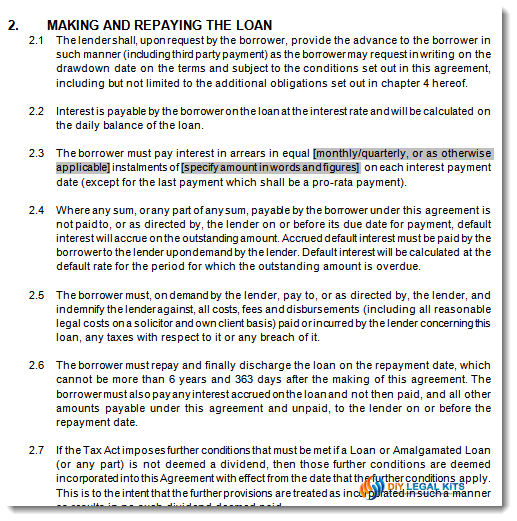

A well-drafted Division 7a Loan Agreement Template is the cornerstone of a compliant loan arrangement. It provides a clear and legally binding record of the terms and conditions of the loan, protecting both the company and the shareholder. The agreement should explicitly address all the requirements outlined by the ATO, leaving no room for ambiguity.

A comprehensive agreement should include, but not be limited to, the following clauses:

Selecting the appropriate Division 7a Loan Agreement Template is critical. There are numerous templates available online, but not all are created equal. It’s important to choose a template that is:

Several sources offer Division 7a loan agreement templates:

Even with a template, several common mistakes can jeopardize the compliance of a Division 7a loan.

Failing to apply the correct minimum interest rate, as determined by the ATO, is a frequent error. The ATO publishes these rates annually, and it’s crucial to use the rate applicable for the relevant income year.

Ambiguous or poorly defined repayment terms can raise red flags with the ATO. The repayment schedule should be clear, specific, and enforceable.

Insufficient documentation, such as a properly executed loan agreement, is a major compliance risk. The agreement should be signed by both parties and retained as evidence of the loan arrangement.

Treating the loan informally, without a formal agreement or adherence to commercial terms, can lead to reclassification as a dividend.

A Division 7a Loan Agreement Template isn’t a “set and forget” document. It’s essential to review and update the agreement periodically, particularly if there are changes to the ATO’s guidelines or the terms of the loan. Annual review is recommended to ensure continued compliance.

Navigating Division 7a loans requires careful planning and meticulous attention to detail. A properly drafted Division 7a Loan Agreement Template is an indispensable tool for ensuring compliance with ATO regulations and avoiding potentially costly tax consequences. By understanding the key requirements, choosing a reliable template, and avoiding common mistakes, businesses and shareholders can leverage the benefits of Division 7a loans while safeguarding their financial interests. Seeking professional advice from a qualified accountant or solicitor is highly recommended to ensure your loan arrangement is fully compliant and tailored to your specific circumstances. Remember, proactive compliance is far more cost-effective than dealing with the repercussions of non-compliance.